While most of Congress is focused on the shutdown turmoil, we have good news to report on the free-market health reform front.

The House Ways and Means Committee yesterday advanced two bills that would give consumers more freedom and flexibility in using their Health Savings Accounts to pay health costs.

The measures would allow more people to create and contribute to an HSA while cutting some of the red tape that makes it more difficult for people to access these tax-advantaged accounts.

“Many of the solutions included in these bills reflect basic common sense,” Ways and Means Committee Chairman Jason Smith said, “such as ending the marriage penalty that currently bars married couples from combining their HSA contributions into a single account, ensuring eligibility of direct primary care arrangements and worksite clinics, and allowing folks to save an amount that will actually cover what they might owe in out-pocket-expenses.”

In addition to increasing the HSA contribution limits, the bills would expand HSA eligibility to Veterans, working seniors on Medicare, Native Americans, and some people enrolled in exchange plans and allow employees to convert their employer-based alphabet soup accounts (i.e., FSAs and HRAs) into a portable HSA they own.

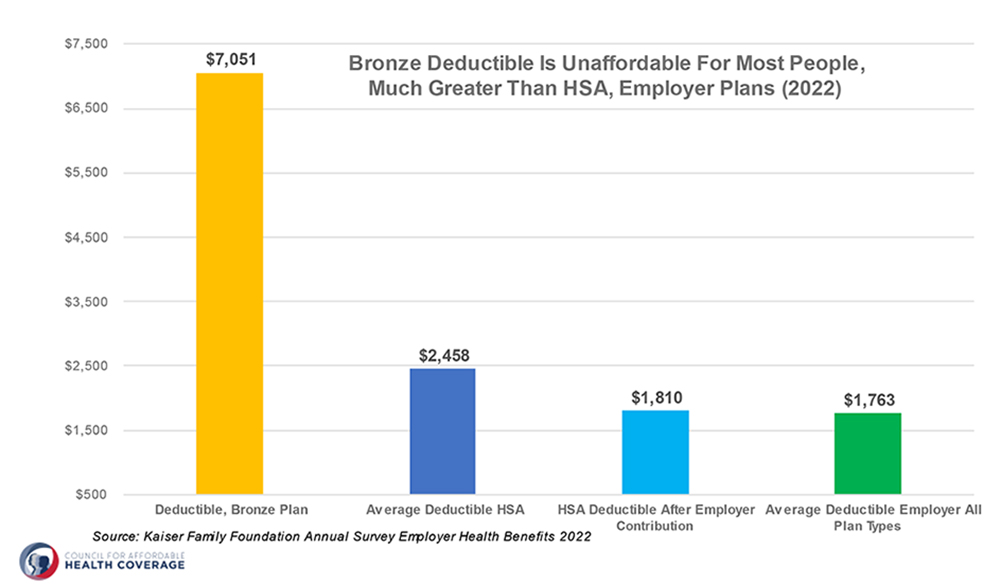

For years, opponents of Health Savings Accounts have said HSAs are just for the healthy and wealthy and have criticized the requirement that people must have a high deductible plan in order to make tax-free contributions to their HSA.

Enter Obamacare, where the average deductible for policies on the ACA exchanges now is $2,000 more than the HSA average. And if a consumer picks the lowest-cost Bronze plan on the ACA, their deductible will be more than $7,000 a year. That’s why so many consumers say their health insurance is virtually useless since they couldn’t afford to pay the deductible if they were to need more than routine medical care.

The Council for Affordable Health Coverage, led by Joel White, supports the bills. “HSAs have been a staple of the health plan market for 20 years, with about 35 million accounts covering 67 million people,” White writes. “Far from being a tax haven for the wealthy, 78% of HSA account holders have a household income of less than $100,000.

“HSAs can fill the gaps not paid by insurance.”

On a related note, the Paragon Health Institute released a report this week Grading the Affordable Care Act and documenting other failings of the ACA, especially the extraordinarily high cost to taxpayers for a program that hasproduced far less enrollment than projected.

“Federal spending on the ACA exchanges…resulted in a total increase of 1.6 million Americans covered under private insurance. The cost to taxpayers has been $36,798 per additional private insurance enrollee which is more than triple CBO’s original projections of $10,538,” authors Daniel Cruz and Greg Fann report.

“The vast majority of individuals who gained coverage following the implementation of the law have done so through Medicaid. Of the 19 million additional Americans with health coverage after the ACA was implemented, 17.4 million were covered under the newly eligible Medicaid expansion group.”

We can do better. We need to stop pouring more and more taxpayer money into the ACA to shore up this failed model and give consumers in a properly functioning market a greater say in their health care choices and spending.

The Ways and Means bills are an important step forward as is the Lower Cost, More Transparency Act that also is poised for House action.